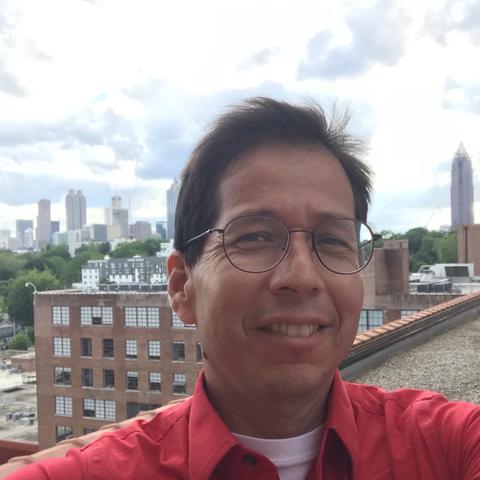

Caption

A park in Savannah's Bingville neighborhood sits flooded on Aug. 7, 2024, from Tropical Storm Debby.

Credit: Benjamin Payne / GPB News

As another tropical system approaches Georgia, many coastal residents are still dealing with the aftermath of flooded homes from Tropical Storm Debby.

They’re also wondering why their streets weren’t included on maps that would have required them to get flood insurance.

Nearly 11 inches of rain fell over four days in Savannah in August, causing widespread flood damage — even in areas deemed at lower risk for flooding.

“It was just an incredible amount of rain over a short period of time,” said researcher Kait Morano of Georgia Tech’s Coastal Equity and Resilience Hub.

Even so, she believes there’s an argument to be made that the disaster was made worse by human-made factors, including huge sprawling developments in Georgia’s fast-growing but low-lying coastal plain and maps of the region produced by the Federal Emergency Management Agency that lulled some residents into a false sense of risk when it comes to coastal flooding.

“Many of the structures that were flooded are outside of FEMA’s flood zones,” Morano said, referring to maps that mortgage lenders must use to determine if a particular property requires flood insurance as a condition of the loan. “Those zones are based on historical data and so people believe that they don’t need flood insurance.”

There are several web-based interactive maps, like this one, produced by Climate Central, that are designed to show the impact of sea level rise.

But Morano suggests residents contact their local flood plain administrators to get a better understanding of their actual flood risk in a particular location.

The decision of whether or not to buy flood insurance is real for residents in ‘X Zones,’ where FEMA doesn’t require flood insurance to secure a loan.

It could add hundreds of dollars per year to the cost of home ownership.

Savannah insurance agent Jeff Brady of Roundtree Brady Insurance Agency said he’ll never suggest NOT buying flood insurance.

“Home insurance does not provide coverage for that,” he said.

But he does suggest using flood insurance pricing as a better indication of risk than just using maps alone.

“With the recent changes to Risk Rating 2.0, which is the FEMA national flood insurance program rating and pricing tool that we use, we’re seeing, from at least a price standpoint, that there are properties, even in ‘X Zones,’ because of their proximity to a flooding source or even the ground elevation associated with it, that they have a greater risk,” he said. “The difference between an ‘X Zone,’ where you’re not required, and an ‘AE Zone,’ where you are, could literally be 1 inch of ground elevation.”

He says one our of every four flood insurance claims come from residents in FEMA zones that did not require flood insurance to secure a loan.