Loading...

Section Branding

Header Content

Welcome to America! Now learn to be in debt

Primary Content

Every time you swipe your credit card for a coffee or a carton of eggs, you take out a tiny loan from your bank.

In many ways, the U.S. runs on borrowed money: a mortgage for a home, financial aid for college, a loan for a car, credit cards for nearly everything else. Over just two years, Americans went from pandemic-fueled, near-record savings to today's highest-ever levels of personal debt.

But what if you were taught to never owe anybody anything?

What may seem like an immigrant cliché actually happens every day: Foreigners arrive in the U.S. with big dreams and a few dollar bills in their wallet. That was true for both of us reporting this story. Tirzah zipped some emergency funds into a hidden compartment of her suitcase; Alina wrapped her college tuition payment into a handkerchief pinned inside her jean pocket.

Cash felt like our proverbial bootstrap, promising the comfort of certainty. But before long, this comfort gave way to a jarring realization:

The U.S. economy counts on you to borrow money and stay in debt.

Almost in a matter of a single generation, America has developed an extensive, even casual reliance on debt. Its epitome is the credit score, which often snares newcomers into a financial Catch-22 — penalizing a lack of debt history and pushing many to take confusing, sometimes costly measures.

When some debt is better than no debt

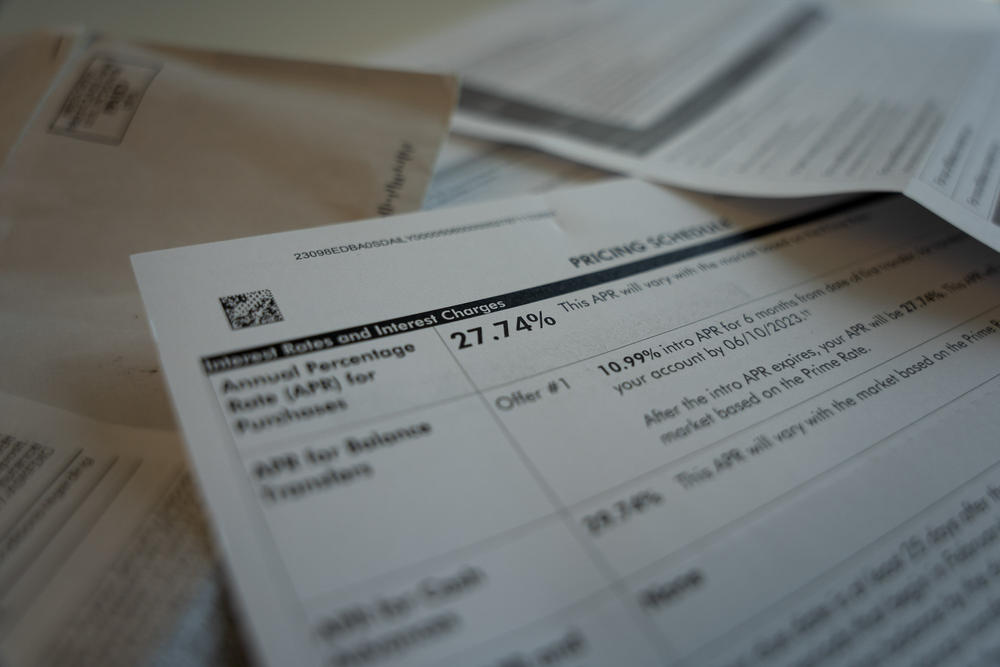

New data this month showed U.S. household debt now surpasses a record $17 trillion. For comparison, the European Union has more households and less than half that amount of debt.

Being financially responsible in the U.S. has come to mean "borrow and repay," says Barbara Kiviat, an economic sociologist at Stanford University.

"It sort of crowds out the idea that maybe not borrowing in the first place is also a good idea," she says. "But we're now living in a world where so much hangs on that credit."

That's because the credit score has become shorthand for how financially trustworthy people think you are — landlords, car dealers, insurance companies, even some employers. The three-digit score is produced by a formula that crunches your debt payment track record; by its standards, being on top of your debt is rewarded, while not having debt at all is a flaw.

To square this idea in her head, Yazmin Lopez had to reconsider what she'd been taught at home.

"Like, my dad — he has all his money under the mattress," says Lopez, who moved to the U.S. from Mexico as a teenager. Her father came up distrusting banks. "He did everything in cash," she says. "He never wanted us to have a credit card."

The two of us remember this dilemma well. Alina's parents — in Russia, in the 1990s and 2000s — bought apartments and cars with cash in a plastic bag. Tirzah's relatives — in India and the United Arab Emirates — cautioned against borrowing anything, let alone money.

"It's such a cultural shift," says Adina Appelbaum, who works with immigrants as a financial counselor and lawyer, "because in many countries they don't have this culture of debt ... and there can actually be shame around having debt or a credit card."

Trapped in a loop without a strong credit history

Without a strong credit history, big things start to get more expensive: car insurance policies, home mortgages, even rent. Landlords might demand extra security deposits or, in Yazmin Lopez's case, simply reject the application, costing her money in lost fees.

Lopez first learned about credit scores from a personal finance book she picked up at Goodwill a few years after coming to the United States. The text described parents building children's credit histories by adding them to credit cards at a young age. Lopez remembers thinking, "Well, that's not going to work."

Even to people born in the U.S., how credit scores work can seem mystifying. Now add to that maybe a language barrier or a cultural one — of generations teaching to avoid debt at any cost. Foreign-born residents — almost 14% of the U.S. population — usually arrive as "credit-invisible," however exceptional their financial history might have been back home.

"I don't know how the credit score is like, scoring," says My Nguyen, a neuroscience student at the University of Illinois Chicago who's from Vietnam. At 20, she's the first in her family to have to sort it out. She wants to qualify for a student loan to attend medical school.

Last July, Nguyen says, her credit card application was rejected by Bank of America. In September, by PNC Bank.

"I was like, I have access to money. I will be able to pay you back everything," Nguyen says. "But I guess I didn't have enough history."

Hearing her story, we both nod. Our banks, too, denied us credit cards at first, despite steady paychecks deposited into savings accounts.

Federal law has long banned discrimination based on national origin, with the Justice Department saying "people cannot be denied equal opportunity because they or their family are from another country." What the banks' credit card rejections often cite is a lack of "revolving trades." Translation: no credit history.

And there it is, the Catch-22: Building a history hinges on getting credit, which in turn seems to hinge on having history.

The scale of the problem

Last year, the Consumer Financial Protection Bureau — a federal watchdog agency — turned its lens on immigrants' financial barriers.

Across the country, the team heard stories of frustration: foreign passports getting rejected as a form of ID, long-term residents struggling to fund small businesses, families squirreling away large sums of money to buy homes, not realizing they couldn't secure mortgages.

"Many financial institutions have policies and practices in place that effectively exclude some immigrants from access to banking services and to credit due to immigration status, even among those with prime or near-prime credit scores," the CFPB's Sonia Lin later wrote in a post.

One of the few federal laws that addresses lending to immigrants — the Community Reinvestment Act — encourages banks to meet the credit needs of people from all income brackets. The effect on foreign-born borrowers is hard to track. U.S. financial watchdogs are working on more financial advice in foreign languages; they rely on immigrants themselves to submit complaints.

In an interview, one CFPB official even shared his own past troubles qualifying for a first U.S. credit card as an immigrant. At least now, he added, more banks have begun pursuing people without credit histories.

In immigrant circles, notes pass from old-timers to newcomers: Did you know you don't have to have a Social Security number to apply for a credit card? Try with a taxpayer ID. Did you see that guy on campus, selling credit cards in a package with cheap international phones? Be careful.

The ultimate tip these days is a secured credit card, the most common exit from the lack-of-history trap. You deposit your own money, say $200, which forms your self-created credit line. The bank tracks your payments and levies any fees. Your credit history ticks up. After half a year or longer, you might reclaim your deposit and graduate to a regular credit card.

How to play the game

Out of all the household debt in the U.S., mortgages account for the biggest chunk, but credit card debt is the most common, approaching $1 trillion. Although modern credit cards are just about 50 years old, 84% of U.S. adults had at least one by 2021.

Stagnating wages contributed to this rapid spread, says Kiviat, the Stanford sociologist. As prices grew and pay languished for decades, credit cards became a common bridge between paychecks.

Another backdrop is ideological: Where other countries might expand government subsidies or benefits, Americans, in a cultural narrative that celebrates self-reliance, tend to tackle social risks with abundant personal borrowing.

"Borrowing money," Princeton University's Andreas Wiedemann writes in his book Indebted Societies, "increasingly determines life chances and full participation as economic citizens."

And credit scores determine just how hard or easy that road will be.

Their history traces back long before credit cards: to retailers in the 1800s, then rampant lending discrimination that remained legal until the 1970s, to becoming a widespread (if criticized) measure of financial responsibility by the 1990s. It wasn't until about 20 years ago that people were able to see their own scores — and soon, getting a good score became such a priority that buying on credit began to feel like it serves a higher purpose.

But this hyperfocus on creating and improving scores, Kiviat writes, "leaves little room for conversations about ... why it is so hard for scoreless (or any other) Americans to get the goods and services they need without resorting to taking on debt."

After her two rejections, My Nguyen eventually got a secured credit card — "a baby credit card," she calls it. She tries to pay off her purchases immediately, just to be safe.

Yazmin Lopez, now 33 and living in Wisconsin, is still dreaming of owning a home, but after years of using a card issued by a credit union, she has started a small business — with its own credit line. And she's now the very parent she once read about: Lopez has added her two children, 8 and 14, to her credit card — building their credit histories and the family's generational wealth.

"I'm glad that I can teach my kids," she says, "that, hey, you can learn how to play the game."

Copyright 2023 NPR. To see more, visit https://www.npr.org.

Bottom Content